The Global Reporting Initiative (GRI) renewed their Universal Standard section last year. Companies that report on their sustainability according to GRI must comply with the renewed GRI reporting standards as of 1 January 2023.

What is the scope of the update? Does this require significant changes to the reporting methods of a company that has reported in compliance with GRI for several years? Please find below my observations and highlights of the changes.

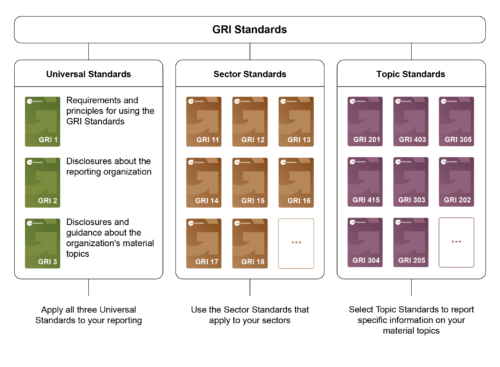

A new structure and sector-specific standards

First, I would like to highlight a practical change. The way standards of the Universal Standard section are grouped and numbered has changed slightly. The Core and Comprehensive options no longer exist.

New sector-specific standards have been introduced and they will be gradually supplemented. The standards offer more detailed instructions for GRI reporting for various sectors and help in identifying key topics.

The first published sector-specific standards are:

- GRI 11: Oil and Gas Sector 2021

- GRI 12: Coal Sector 2022 and

- GRI 13: Agriculture, Aquaculture and Fishing Sectors 2022 which was published very recently.

The Topic Standards section will remain unchanged although individual standards will be updated as before. With these, you simply have to check the year to make sure you are using the most recent Topic Standard.

Source: https://www.globalreporting.org/media/s4cp0oth/gri-gristandards-visuals-fig1_family-2021-print-v19-01.png

GRI 1 and impact

The GRI 1 – Foundation 2021 replaces the GRI 101 Foundation 2016 standard. The GRI 1: Foundation 2021 is the very first document you should read before diving into GRI reporting. It defines the principles of GRI reporting.

Key changes include a new definition of impact and increased importance of due diligence.

Impact refers to the effect the organisation has or could have on the economy, environment and people. This does not refer to the term “social responsibility” but rather focuses on any impact on people, which automatically includes all effects on the realisation of human rights. The definition refers to effects caused either directly by the organisation’s action or through their business relationships.

The standard defines due diligence as a process through which the organisation identifies, prevents, mitigates and reports the organisation’s actual or possible negative impacts on the economy, environment and people, including all human rights impacts.

The standard also includes a clearer description of the GRI reporting process.

GRI 2 and more comprehensive administrative reporting

GRI 2 – General disclosures replaces the GRI 102 General Disclosures 2016 standard. GRI 2 includes a list of reporting topics, such as the organisational, sustainability management, sustainability principles and reporting practices.

GRI reporting now requires that all of the topics listed in the standard are included in the sustainability report. The reporting topics have also been slightly modified and the management of corporate responsibility must be reported more comprehensively.

GRI 3 and most significant impacts

GRI 3 Material topics 2021 replaces the GRI 103 Management Approach 2016 standard. The updated standard defines in more detail what a material topic refers to, how they can be identified and how they should be reported on.

The updated standard emphasises that material topics are those that represent the organisation’s most significant impacts on the economy, environment and people, including impacts on human rights. The organisation must report its most significant positive and negative impacts, both actual and potential. When identifying impacts an organisation must take into consideration both those directly created by the organisation as well as impacts caused through business relationships.

The most significant impacts are prioritised by analysing them from the perspective of seriousness and likelihood. It should be noted that GRI reporting does not require drawing up a materiality matrix, but only the comprehensive identification of material topics.

The updated standard also defines how to utilise the new sector-specific Sector Standards in identifying material topics. If a GRI Sector Standard exists for the organisation’s sector, the organisation must utilise it in their reporting.

The identification and management of material topics follows mostly the same principles as the UN Guiding Principles on Business and Human Rights.

So, what actually changes in GRI reporting?

GRI has stated that objective of the update is to strengthen the transparency of communication and better meet stakeholders’ information needs.

A significant change in GRI reporting is modifying the definition of material topics and reporting obligations so that the organisation is under obligation to report its most significant impact on people, nature and the economy, not on the organisation itself.

The standard places emphasis on identifying and reporting impacts on human rights. Any impact an organisation has on people will always include an impact on human rights. In addition, the standard highlights management and reporting: what action will the organisation take once it has identified impacts?

This update may sound small, but it is quite significant. GRI reporting steers the organisation to identify and manage its significant impacts on people, nature and the economy in the entire value chain.

This means that you should prepare sufficiently for reporting in accordance with the updated Universal Standard section.

**

Tofuture’s cloud-based tool allows organisations to systematically gather sustainability data to meet the needs of GRI reporting. The tool is a GRI-certified software programme. Get in touch!